| Welcome to the weekend. You survived Valentine’s Day, likely celebrated Presidents’ Day as much as anyone celebrates Presidents’ Day, and made it through another noisy week. Bravo. You might notice we’re coming at you with a fresh look this week. Stay tuned for even bigger and better changes in the weeks ahead. | |

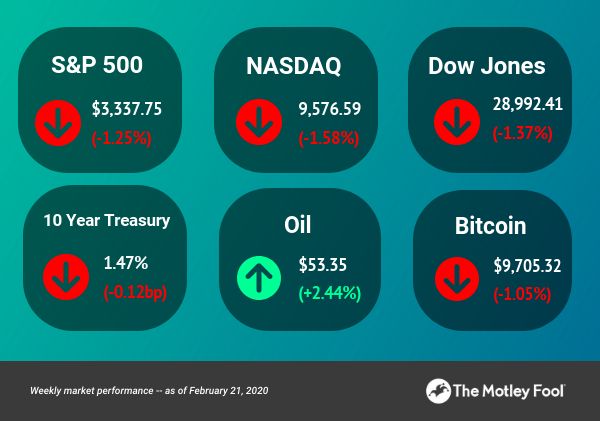

WEEKLY MARKET PERFORMANCE | | GLOBAL MARKETS In Europe, Sharing is Caring The EU’s not playing around. Margrethe Vestager, the European Commissioner for Competition, put forward a proposal that will put even more restrictions on how the largest (American) tech companies operate in the continent. - To be clear, nothing is set in stone… yet. The riveting regulatory details will get hammered out in the following months.

- The primary focus is data, specifically a push for the tech titans to share the proprietary data that entrenches their monopolistic(ish) advantages. The commission is the angstiest about antitrust, but new rules could also affect how companies build their algorithms and are held liable for content users publish on their platforms.

- In Vestager’s eyes, tearing down walled gardens and democratizing access to certain data will lead to a more even competitive playing field. If “unfair” data advantages are reduced, then other European companies will be able to more effectively innovate.

So what? First, there was GDPR. Then Alphabet was fined billions of euros three(!) times for various “abusive” practices. And both Amazon and Apple are trying to weasel out of their own EU fines. In other words, it’s a fun time to be a massive and massively profitable corporation that consumers love but politicians love to hate. Legacy regulations fail to apply to today’s internet-driven world, so it’s simply inevitable that new internet regulations will stir up commotion for many years to come. Will it result in the downfall of these mega-companies? Nope. Will it be noisy and annoying? Yep. Will it unlock European innovation? TBD.

| | M&A How to E*Buy 5 Million New Customers Remember Black Tuesday? Oh no, that other slightly less dramatic Tuesday. On October 1st of last year, Charles Schwab announced it would slash its online commissions on stocks, ETFs, and options to zero, zilch, and nada. The ripple effects were immediate: stocks of other brokerage businesses plummeted on the new reality that they need to quickly match Schwab’s pricing or lose customers. It also signaled a paradigm shift. Brokerages would now compete based on other services (loans, investment advisors, etc.), which incentivizes consolidation as a means of seeking efficient scale. Schwab quickly scooped up TD Ameritrade, but the dominoes continue to fall. - Morgan Stanley is acquiring E*Trade for approximately $13 billion in an all-stock deal. That’s the largest acquisition by a US bank since the Great Recession. Wowza.

- Put in perspective, Morgan Stanley has 3 million clients with $2.7 trillion in client assets (about about $900,000 per client). E*Trade's has 5.2 million accounts with $360 billion in assets (just under $70,000 per client). These are very different clienteles.

- As much as everyone loves to hate on synergy, there’s some truth to it here. As E*Trade users age and grow their wealth, the combined company will more easily upsell them to more premium wealth management services. Plus, there’s almost certainly room to cut duplicate costs.

It doesn’t make no sense. E*Trade on its own would struggle to compete against larger brokerages, and Morgan Stanley would benefit from expanding its service suite. Although Morgan Stanley is nowhere close to its pre-recession highs, business has improved over the past few years, and a rising stock price makes stock-based deals more rational. Consolidation should strengthen both businesses, but whether the combined entity can effectively compete with the Charles Schwabs and Fidelitys of the world remains an unanswered question. | | ENTERTAINMENT Our New National Pastime: Cord Cutting The numbers are rolling in and they’re… ugly. According to the WSJ, 3.2 million pay-TV subscribers cut the cord in 2018, and over 5.5 million did so in 2019. That represents an 8% drop for the largest cable and satellite companies, bringing the total number of US cable subscribers to approximately 83 million. - Despite snowballing unsubscribes, 83 is a lot of millions. There are 128 million domestic households, so roughly 65% of homes still use traditional pay-TV. Cord cutting has a long way to go.

- Companies like AT&T and Comcast are adapting. Rising programming costs translate to higher customer bills, which contributes to churn. However, instead of lowering prices to better retain customers, companies are refocusing on broadband services. Nearly as many households now pay for broadband as pay for cable or satellite TV.

- Skinny bundles — those cheaper, slimmed down, “over-the-top” offerings — have a place. First-movers (like SlingTV) are losing market share mostly to Hulu + Live TV and YouTube TV. That said, rising prices could slow everyone’s roll.

Something doesn’t add up. Programming costs are rising and traditional TV ad spend remains near all-time highs… yet pay-TV subscribers are falling off a cliff. It’s a recipe for unsustainability. As cable evolves to more closely resembles a live sports bundle, passionate fans will continue to pay up for “can’t miss” content, but pricing may need to recalibrate. Hello, Captain Obvious. Streaming is the future. If the 2010s was about laying the streaming foundation, the 2020s is about converting everyone. Netflix will continue to make a dent, Disney is building a remarkable ecosystem, and a long-tail of other services will certainly add up. People talk about the streaming wars, but it’s really a misnomer. The war is primarily against traditional TV, and there's a significant amount of land left to grab. | |

STOCKS This Week’s Pops and Drops - Dominos leaped 25% on Thursday on better than expected sales and earnings, showing this pizza maker still has the sauce.

- Groupon’s latest results were reeeeeally bad: revenue fell 23%, and the company announced it’s exiting the goods category, sending stock down over 40%.

- L Brands is taking Victoria’s Secret private (via private equity) for only $1.1 billion, and founder / CEO Leslie Wexler is stepping down. A quintessential fallen angel.

- Six Flags is currently like a rollercoaster that only goes down, and a horrible fourth quarter didn’t help. Attendance mildly rose, but guest spending fell and earnings crashed, forcing the company to cut its dividend by 70%.

- Stamps.com. Name a crazier stock over the past 12 months. I’ll wait. Despite two 50% drops, Stamps — an online postage seller — found a way to quintuple off its lows. Thursday’s 65% jump on news that it beat quarterly expectations and formed new agreements with UPS and the USPS certainly helps.

- Virgin Galactic is the only publicly traded space tourism business — up 32% this week and 300%+ since its October IPO — and it’s suddenly one of the most traded stocks in the market. Fascinating, but how’s business? Err… nothing to show yet but lots to look forward to.

- Zillow popped on Thursday as results indicate its plan to transform how homes are bought and sold is working as planned.

| | The Business of Baby Yoda | | | “Everybody needs money. That’s why they call it money.” Investors Ron Gross, Jason Moser, and Jeff Fischer join host Chris Hill to discuss retail, food, space, and toys — not to mention their Radar Stocks. Plus, toy expert Chris Byrne analyzes the current state of the industry and the business of Baby Yoda. If you don’t listen, you’re basically admitting you hate Baby Yoda. Check it out: Apple Podcasts, Spotify, wherever. | | | | |

No comments:

Post a Comment