| AT&T Stock: Ma Bell Belongs In An Income Investor’s Portfolio Posted: 08 Jun 2019 11:44 AM PDT Hits: 6

Stocks are having another roller coaster week and, in this volatile market, many investors are increasingly looking to generate relatively safe passive income from dividend-paying stocks. If that sounds like you, then you may want to read on. Today I'd like to discuss the short- and long-term outlook for AT&T (NYSE:T) stock.  Source: Shutterstock Although I believe T stock belongs in a long-term income-generating portfolio, I expect market volatility to continue in June. Therefore, we can expect price choppiness in AT&T stock, too. With the shares down about 6% since May 20, any further pullbacks in the coming weeks would be a sign to investors to consider buying into the shares. With that said, let's take a deeper look into what makes T stock a good long-term investment. Diversified Revenue Stream AT&T reported Q1 2019 earnings on April 24. With a market capitalization of $230 billion, the Dallas-based group breaks down revenue into six main segments. - Mobility (includes wireless subscribers)

- Entertainment Group (includes DirecTV and U-Verse customers)

- Business Wireless (provides services to companies and the government)

- Latin America (includes Latin American and Mexican operations)

- Warner Media (includes HBO, Turner and Warner Bros.)

- Xandr (handles all advertising business)

AT&T's domestic wireless business is neck and neck with Verizon Communications (NYSE:VZ) for market share. In June 2018, a federal court approved the merger of AT&T's $85 billion acquisition of Time Warner — a deal that has turned AT&T in a media giant and "content king." This merger has been weighing on T stock price for some time; however, the rest of 2019 should see the question marks slowly disappear. As internet-based communication becomes increasingly integrated into our daily lives, I find AT&T shares well-positioned to benefit from various commercial opportunities that would eventually benefit the share price. AT&T Stock Has Strong 5G Prospects Over the past few years, T stock has lagged behind the broader market. Yet, the company has a strong brand and wireless infrastructure — two factors that are likely to make it a dominant player in the 5G sphere. The new 5G technology will boost productivity and growth globally. 5G will also be at the center of the infrastructure for building smart cities. Coupled with a trailing price-to-earnings ratio of about 12x, T stock deserves further due diligence in the tech world that is getting ready for 5G dominance. In December 2018, AT&T launched its own 5G network in over a dozen U.S. cities. It is the second major telecommunications provider to do so after Verizon. The first wave of 5G cities includes Atlanta, Charlotte, Raleigh, Dallas, Houston, Indianapolis, Jacksonville, Louisville, Oklahoma City, New Orleans, San Antonio, and Waco, Texas. T Stock's Improving Balance Sheet Most long-term investors do not want to be constantly thinking about the fundamental strength of the stocks in their portfolios. AT&T's balance sheet has been improving in recent quarters — another reason why I am interested in T shares long-term. The improving fundamentals are possibly why AT&T stock price has gone up even though the company posted a subdued quarterly report. The company's key Mobility wireless segment generated revenue of $17.57 million, up 1.2% year-over-year. And the company achieved 80,000 postpaid phone net adds vs. 49,000 postpaid net adds in the year-ago quarter. Wall Street welcomed the news that the mobility segment has increased revenue. On a final note, over the past few quarters, AT&T's debt load has been on Wall Street's radar. The company finished 2018 with a debt load of $171 billion. Acquiring Time Warner has bloated this debt load. However, the communications giant is now working to cut costs and the debt at the same time. For example, it has recently sold its minority stake in Hulu, a premium streaming service, to its other owners Walt Disney (NYSE:DIS) and Comcast (NASDAQ:CMCSA), for almost $1.5 billion. Management realizes the importance of decreasing the level of debt sooner than later. Therefore, I am still comfortable with this amount on the books. AT&T Stock Dividends In general, big blue-chip names tend to be consistently generous dividend payers. And telecommunications companies have traditionally been seen as relatively safe dividend investments. One such income-investor favorite has been T stock. Experienced dividend investors also pay close attention to a company's free cash flow as dividends are ultimately paid out of cash. AT&T is a large business that generates a lot of cash. The group has recently confirmed that it will have about $26 billion in free cash flow this year. In addition to the company's strong earnings power through telecom and media-related operations, T stock also offers a strong dividend yield at over 6.5%, which is a big attraction for many long-term investors seeking strong stocks to buy for 2019 and beyond. Finally, over the past 35 years, AT&T has a history of increasing dividends annually. This is yet another important reason why I believe T stock belongs in a capital-growth portfolio. As long as investors still believe in T stock's prospects, the hefty dividend yield keeps them from panicking and selling the shares. Should You Buy AT&T Stock in June? Many stocks may continue to be volatile in June, and I would not advocate trying to identify stocks that could be immune to a U.S.-China trade war. T stock is likely to range trade with a downward bias, possibly until its next earnings report in late July. Yet if AT&T stock price declines further, especially toward $27.50, long-term investors may find it particularly attractive. If you aren't already long T stock, you may want to remain on the sidelines and wait for a pullback. I'd also consider buying covered calls in conjunction with going long on AT&T shares. Consider that Wall Street regards telecoms' revenues to be relatively safe during an economic slowdown, since not many people would give up their phone account in a slowdown, unless their personal economic situation got really bad. But creating growth opportunities in a mature industry like telecommunication services still requires proactive management, like that of AT&T. The 5G revolution should also be a strong catalyst for the stock price. Therefore, despite any potential short-term price weakness, T stock belongs to a diversified portfolio. Amid all the recent market volatility, I regard AT&T as one of the key telecom stocks to buy for value and stability. As of this writing, Tezcan Gecgil did not hold a position in any of the aforementioned securities. Can you get rich from fx trading? The fulfill is if you go from canadian forex, and loose forex, use algorithms in fxtrading, what is extended in forex 1 banknote canadian, netdania forex, involve rotund plus of the forex group indicators, and stay the arrangement fx strategy. We instrument succeed win all. Can you get gilded from fx trading? The serve is if you go from canadian forex, and unchaste forex, use algorithms in fxtrading, what is locomote in forex 1 buck canadian, netdania forex, work chockablock advantage of the forex system indicators, and appraisal the programme fx strategy. We testament succeed win all.

Top 10 problems you may need in life:

01. Espresso Machines review|

02. Gaming Keyboards review|

03. Gaming Headsets review|

04. Virtual Reality Headsets review|

05. Cordless Drills review|

06. Electric Keyboards review|

07. Gaming Mouse review|

08. Gaming Monitors review|

09. Gaming Laptops review|

10. WiFi Routers review|

|

| Say goodbye Apple. New stock could be 40X better Posted: 08 Jun 2019 11:32 AM PDT Hits: 8

<!–[if (gte mso 9)|(IE)]> <![endif]–> | | <!–[if (gte mso 9)|(IE)]> <![endif]–> | | If you own Apple’s stock, know someone who does, or have even thought about buying it… there’s something you need to know. You see, there could be a king’s ransom up for grabs as what could be Apple’s next game-changer makes its way outside of the company’s secretive design labs in Silicon Valley. But, we think one stock that’s poised to benefit the most from Apple’s next game-changer IS NOT Apple. Yes, some of the biggest names on Wall Street are calling for once-in-a-decade opportunity for Apple. Analysts at Morgan Stanley report many investors are "still underestimating" the coming "iPhone Supercycle." Forbes is calling it an "iPhone tsunami." So, yes, Apple is set to sell hundreds of millions of new iPhones. But you already knew that. What most people don’t know is tech insiders think there’s an invaluable, tiny component inside Apple’s newest iPhone that Apple doesn’t manufacture in-house! They don’t make it because they don’t have the technology OR the patents to do so. That’s because another company (1/100th of Apple’s size) owns the rights to those patents — so Apple would have to pay that company to include its technology in their gadgets. Translation: This tiny company essentially gets paid every time Apple sells their revolutionary new iPhone. You don’t have to be a numbers-whiz to understand what that kind of growth can do to a company’s stock price. That’s why I hope you take a few minutes to unlock the full research a team of highly trained stock analysts from The Motley Fool put together on this developing story and discover why we could be near a turning point. Click below to get all of the details and the name of this stock poised to take-off. Don’t wait until the name of this company is on everyone’s lips. By Clicking you agree to Receive Email Updates and

Special Offers from The Motley Fool Here’s to you and your family’s wealth, David Hanson

Investment Analyst,

The Motley Fool |   | | <!–[if (gte mso 9)|(IE)]> | <![endif]–> | | | <!–[if (gte mso 9)|(IE)]> <![endif]–> | This is a PAID ADVERTISEMENT provided to customers of Schaeffer’s Investment Research. Although we have sent you this email, Schaeffer’s does not specifically endorse this product nor is it responsible for the content of this advertisement. Furthermore, we make no guarantee or warranty about what is advertised above. Your privacy is very important to us, if you wish to be excluded from future notices, do not reply to this message. Instead, please click here. Schaeffer’s Investment Research

5151 Pfeiffer Road, Suite 250

Cincinnati, Ohio 45242 Privacy Policy | <!–[if (gte mso 9)|(IE)]> | <![endif]–> | <!–[if (gte mso 9)|(IE)]> | <![endif]–> |

2019-06-08 13:40:17

Source link Can you get moneyed from fx trading? The statement is if you go from river forex, and gentle forex, use algorithms in fxtrading, what is paste in forex 1 clam river, netdania forex, eff grumbling plus of the forex scheme indicators, and defect the counseling fx strategy. We module win win all.

Top 10 problems you may need in life:

01. Espresso Machines review|

02. Gaming Keyboards review|

03. Gaming Headsets review|

04. Virtual Reality Headsets review|

05. Cordless Drills review|

06. Electric Keyboards review|

07. Gaming Mouse review|

08. Gaming Monitors review|

09. Gaming Laptops review|

10. WiFi Routers review|

| | Current Weakness in MongoDB Just Makes MDB Stock a Better Buy Posted: 08 Jun 2019 11:08 AM PDT Hits: 13

Shares of high flying technology stock MongoDB (NASDAQ:MDB) traded lower in early June after the company reported strong first quarter numbers, but delivered sub-par second quarter and fiscal 2020 profit guides. Because MDB stock was so richly valued heading into the print, the stock naturally dropped in response to the slightly disappointing guides.  Source: Shutterstock This reset is perfectly normal, healthy and nothing to worry about in the big picture. In that big picture, MDB stock will continue to fly high because MongoDB finds itself supported by exceptionally favorable growth fundamentals, which ultimately pave the path for this company to one day be really big, really profitable, and really valuable. Thus, for long term investors, near term weakness in MDB stock should be consistently viewed as a buying opportunity, so long as the growth rates remain big, the margins remain high, the valuation remains reasonable, and the macro backdrop remains favorable. Right now, all three of those boxes are checked off for MDB. Consequently, current weakness in the stock should be perceived as a buying opportunity. MongoDB Is Oozing with Long Term Growth Potential The story at MongoDB is pretty easy to understand, and it is one that lends itself to tremendous long term growth potential. At the heart of every software application is a database. That database is used to store, organize, and process data. Traditionally, these databases were relational, meaning they were row-based. That's because traditional data was almost always structured in a row-column manner. But, modern data isn't always structured as such. In fact, because we can now generate data through various channels, modern data is increasingly document-based and much more free-flowing. Enterprises need to store, organize, and process this document-based data, too. But, relational databases can't do that efficiently. As such, there's been a boom in the adoption of non-relational databases to handle this new data form. MongoDB is one of these non-relational databases, but it's different in one important way: It's a hybrid database that combines the best aspects of non-relational and relational databases so that enterprises can handle all data formats. This solution has been a huge hit. MongoDB has consistently grown revenues and customers at a 50%-plus rate over the past several years, with growth actually accelerating over the past several quarters thanks to more and more businesses understanding the benefit of a hybrid database solution. The potential here is that MongoDB has just 14,200 customers. There are nearly 6 million employer businesses in the U.S. alone. Further, the company projects to do just $380 million in sales this year. The global software database market is closing in on $60 billion. Broadly, then, MongoDB is a hyper-growth tech company, with a winning solution, that is rapidly gaining share in a big market, and which has a very long runway for future growth. That is a winning combination for MDB stock. The Growth Boxes Are Checked Off When it comes to long term winners like MDB, you want to buy them on weakness so long as all the growth boxes are checked off. Those growth boxes include: 1) still healthy revenue growth, 2) stable margins, 3) reasonable valuation 4) favorable backdrop The Q1 report confirmed that MongoDB stock does check off all those boxes. Revenue rose 78% in the quarter, which is substantially above the company's multi-year revenue growth trend. Revenue growth is projected to remain very big for the foreseeable future, too. Customer growth trends likewise remain healthy. Total customers were up more than 100% in the quarter. Gross margins are taking a step back. But, that's because of some new business integration issues which will pass by the end of the year. Meanwhile, operating margins are substantially improving as robust revenue growth is driving equally robust opex leverage. The valuation is rich. But, assuming this company can grow revenues at a 20%-plus rate over the next decade, maintain 70% gross margins, and drive the opex rate down to 30%, MongoDB could easily be looking at $10-plus in EPS by 2030. A big growth average 30-forward multiple on that implies a 2029 price target for MDB stock of $300 or more. So, long term upside remains compelling. Lastly, the backdrop is still favorable. This company has minimal trade exposure because it's a services business. An economic slowdown does pose a threat, but the secular pivot towards hybrid databases is likely strong enough to offset such weakness. Meanwhile, new data is increasingly not in a row-column format. Companies are also increasingly adopting data-driven growth strategies. Thus, the need for an enterprise to adopt hybrid databases is only growing. All in all, the current trends here remain favorable. Bottom Line on MDB Stock MDB stock is a long term winner that continues to be supported by favorable growth trends. So long as that remains true and the valuation remains reasonable in the big picture then MDB should remain on a medium to long term uptrend. Against the backdrop of that medium to long term uptrend, near term weakness is a buying opportunity. As of this writing, Luke Lango was long MDB. Can you get rich from fx trading? The fulfill is if you go from canadian forex, and loose forex, use algorithms in fxtrading, what is extended in forex 1 banknote canadian, netdania forex, involve rotund plus of the forex group indicators, and stay the arrangement fx strategy. We instrument succeed win all. Can you get gilded from fx trading? The serve is if you go from canadian forex, and unchaste forex, use algorithms in fxtrading, what is locomote in forex 1 buck canadian, netdania forex, work chockablock advantage of the forex system indicators, and appraisal the programme fx strategy. We testament succeed win all.

Top 10 problems you may need in life:

01. Espresso Machines review|

02. Gaming Keyboards review|

03. Gaming Headsets review|

04. Virtual Reality Headsets review|

05. Cordless Drills review|

06. Electric Keyboards review|

07. Gaming Mouse review|

08. Gaming Monitors review|

09. Gaming Laptops review|

10. WiFi Routers review|

| | May leaves, and the Brexit case lives: in the EU, they are talking about a new postponement Posted: 08 Jun 2019 11:01 AM PDT Hits: 20

Today, Theresa May is leaving the post of leader of the Conservative Party, fulfilling her promise, announced at the end of May. However, for the time being, she has lost only her political position – until the moment when her successor is determined, May will serve as the acting Prime Minister of Britain. The pound played this fact two weeks ago, so today it calmly and phlegmatically reacted to predictable changes. Traders are now concerned about another question: who will replace May and how will he (or she) build relations with Brussels, taking into account the coming “X hour” on October 31? Despite the summer period, the political struggle is in full swing, although the election campaign will officially begin only three days after the resignation of the Prime Minister from the post of leader of the ruling party, that is, on June 10. Nevertheless, there are already unconditional favorites of the political race and obvious outsiders. Among the first – Boris Johnson and Dominic Raab. They take a rather tough position on further relations with Europe and allow the option of “hard” Brexit. In addition, they oppose the extension of the negotiation period after October 31. In particular, Johnson has repeatedly stated in his speeches that the country will, in any case, withdraw from the Alliance on the last day of October – with or without a deal. This fact has a strong background pressure on the GBP/USD pair – even taking into account the weakening dollar, the price fluctuates in the range of 25-27 figures. However, the question of a possible (next) delay is being discussed now, despite Johnson’s categorical stance on this matter. Both in Europe and Britain understand that the most likely candidates for the Prime Minister’s post are not ready to make significant concessions to Europeans, while the Europeans themselves refuse in principle to revise the terms of the agreed deal. That is, in the autumn, the situation will again go into a political impasse, where there are two ways out: either a hard Brexit or a new delay. Johnson’s pre-election bragging about being ready for a chaotic scenario can be replaced by a certain caution when it comes directly to the implementation of this option. Theresa May once say in the same way that “the absence of a deal is better than a bad deal”, but in the end, she did not dare to send the country down the slope by hard Brexit. And there are not so many “hawks” in the Parliament who are ready to admit such an option – the results of the signal votes that were held at the beginning of this year, eloquently testify to this. That is why experts are now discussing a burning question: how long will Britain be in limbo, and how long the European Union agrees to tolerate the British under its wing. According to the British press, most EU governments believe that Britain should leave the Alliance no later than June 2020. This is due to the fact that next summer, the EU will discuss a 7-year budget plan. Until January 1, 2021, all key authorities of the European Union must finally accept and approve this document. However, not all EU countries are ready to provide such a long delay. Initially, the Germans opposed this option. Members of the Bundestag said that Germany will veto another Brexit delay if Britain does not hold a general election or a second referendum. Immediately, it is worth noting that neither Johnson nor Raab will not agree to the implementation of this ultimatum. Another country of the European Union – France – voiced the same conditions, however, in a somewhat veiled form. French President Emmanuel Macron recently said that the deadline is the deadline for the implementation of Brexit, and he personally opposed the provision of any new delays.

Here, it should be emphasized that such harsh public statements by politicians of the first-tier cannot be taken at face value. Such threats and ultimatums have been heard before. The purpose of this rhetoric – to spur British politicians to action and increase the pressure on them. Although in fact, the British and Europeans believe hard Brexit to be “economic suicide”. So, according to one influential British newspaper, in fact, the European Union is ready to give London a new delay if the British authorities cannot approve the terms of the transaction until October 31. As assured journalists of their information sources, at least 25 EU member states agree to provide the country with such an opportunity. This publication today provided support to the British currency – the GBP/USD pair was able to gain a foothold in the 27th figure. Although the information is unofficial, the market decided that “there is no smoke without fire”. By the way, such rumors find a response among British politicians. In particular, the candidate for the post of leader of the Conservative party (and thus the Prime Minister) Michael Gove yesterday told Cabinet members that he was ready to postpone Brexit from October this year until the end of next year. Gove is not a favorite of the political race, so the pound actually ignored his words. But if such an idea is expressed by Boris Johnson (or Raab), the British currency will get a reason for a more significant correction – up to the level of 1.2860, where the upper line of the Bollinger Bands indicator on the daily chart coincides with the Kijun-Sen line. The material has been provided by InstaForex Company – www.instaforex.com

2019-06-07 15:30:42

Source link Can you get moneyed from fx trading? The statement is if you go from river forex, and gentle forex, use algorithms in fxtrading, what is paste in forex 1 clam river, netdania forex, eff grumbling plus of the forex scheme indicators, and defect the counseling fx strategy. We module win win all.

Top 10 problems you may need in life:

01. Espresso Machines review|

02. Gaming Keyboards review|

03. Gaming Headsets review|

04. Virtual Reality Headsets review|

05. Cordless Drills review|

06. Electric Keyboards review|

07. Gaming Mouse review|

08. Gaming Monitors review|

09. Gaming Laptops review|

10. WiFi Routers review|

| | HBO, Game of Thrones and the AT&T Stock Price Posted: 08 Jun 2019 10:31 AM PDT Hits: 35

There's no shortage of worries when it comes to AT&T (NYSE:T). The T stock price hasn't moved in years. In fact, shares touched a seven-year low in December, and trade below where they did at the beginning of 1998. AT&T is the most indebted company in the world. Growth remains meager.

Indeed, I've been a longtime skeptic toward T stock. I argued as recently as last month that shares should sit below $30. From a broad standpoint, the concern is that AT&T simply isn't winning. In Mobility, the company is losing market share to Verizon Communications (NYSE:VZ) and T-Mobile (NASDAQ:TMUS). The Time Warner acquisition remains reliant on the Turner networks — likely victims of cord-cutting. DirecTV is hemorrhaging subscribers. The streaming service is late to market, and seems to have little chance of dislocating Netflix (NASDAQ:NFLX) and Hulu, let alone the coming offering from Disney (NYSE:DIS). A little over two weeks after the finale of HBO's Game of Thrones, some investors have added that network to the list of worries. Will subscribers abandon the network, which potentially is AT&T's most attractive asset? Did poor reviews for the finale undercut future opportunities for the franchise? They are interesting questions from a business standpoint. But in fact, Game of Thrones — and even HBO — aren't necessarily that material to the AT&T stock price. That's good news, but it's also part of the problem. Game of Thrones and T Stock Viewers did not enjoy the GoT finale, or even the last season. As Vox pointed out, the finale has far and away the lowest rating on IMDB of any episode in the series. A petition at Change.org to remake the final season "with competent writers" has received 1.6 million signatories. Game of Thrones hasn't yet really moved T stock. Indeed, despite initial backlash to the ending, shares actually increased modestly the next day. But that hasn't stopped market participants from voicing concern about the franchise, and its impact on HBO. Most notably, without GoT, HBO doesn't have a headline blockbuster series with which to attract subscribers. The finale itself set a record as the most-watched HBO show ever. That's a truly impressive accomplishment in a time of increasing audience fragmentation. No doubt some of the 19 million viewers are subscribers who are now at risk of canceling. HBO could, of course, keep or win back those subscribers with expansions to the GoT universe. Three successor shows reportedly are in the works. But the disappointment of the finale might keep those viewers from returning. And it's that risk that could weigh on T stock. At Marketwatch, columnist Brett Arends went as far as to breathlessly argue that AT&T shareholders would have a case to sue the company. "AT&T's management has just needlessly thrown away a prize asset for no good reason," he wrote in arguing against the decision to even end the series. Arends compared that decision to the infamous "New Coke" rollout by Coca-Cola (NYSE:KO) back in the 1980s. Meanwhile, after the apparently disappointing season, the new offerings are now tainted. "The question now is whether the franchise has much magic left anyway," he added. Does HBO Matter to the AT&T Stock Price? Arends furthered his point by noting that AT&T CEO Randall Stephenson specifically called out HBO and GoT in justifying the $85 billion acquisition of Time Warner back in 2016. From that standpoint, the GoT misstep — if it was a misstep — presents a real risk to AT&T stock. And subscriber losses are a risk. HBO's direct subscribers contribute some $15 per month, or $180 per year in revenue each. Incremental subscribers are gained and lost at exceedingly high margins. The cost of adding a subscriber is minimal: it doesn't make HBO's programs more expensive, and incremental infrastructure costs are modest as well. But the reverse is true of losing a subscriber: most of the revenue dollars fall away from profits. All that said, HBO is only a small part of the AT&T empire. In the first quarter, according to figures from the 10-Q, HBO contributed just 5.6% of total segment-level profit. EBITDA is in the range of $2.4 billion annually. Two factors do amplify the importance of HBO to T stock. First, the company has a tremendous amount of debt. And so, HBO's contribution to the equity is more important than its contribution to the business. Take away HBO's profits, all else equal, and the T stock price would drop close to 10%. Secondly, HBO is probably the most expensive asset AT&T has. The $2.4 billion in EBITDA suggests the business could be worth as much as $25 billion. That's assuming a 12x EBITDA multiple, and that a standalone HBO would have some level of corporate costs. That figure is a little over 10% of the current market capitalization of $231 billion. HBO Is Neither Catalyst nor Headwind for AT&T Still, modest or even significant erosion in HBO subscribers doesn't necessarily mean enormous downside for AT&T stock. Even the loss of five million subscribers — nearly 25% of the GoT finale viewers — would only hit revenue by about $900 million. Full-year segment-level profit should be over $40 billion. While that might seem like good news in the context of AT&T stock, it also currently highlights the broad problem. HBO truly is AT&T's most impressive asset. It would be hugely in demand if the company were to sell it (though it obviously won't). Also, the markets would dearly value the network if the company spun it off. Yet AT&T's most impressive asset doesn't matter all that much in the context of the total business. Wireless will ultimately drive T stock, where market growth is minimal and AT&T's share is shrinking. The merger between Sprint (NYSE:S) and T-Mobile could help, though the forced sale of Boost Mobile might mean a fourth large player like Comcast (NASDAQ:CMCSA) joins the industry. Other key contributions come from Turner and DirecTV, both of which likely are in secular decline. Subscriber losses at HBO won't help the cause, to be sure. But they simply don't change the case all that much. HBO isn't going to move T stock significantly, which raises the question of what actually will. As of this writing, Vince Martin has no positions in any securities mentioned. Can you get rich from fx trading? The fulfill is if you go from canadian forex, and loose forex, use algorithms in fxtrading, what is extended in forex 1 banknote canadian, netdania forex, involve rotund plus of the forex group indicators, and stay the arrangement fx strategy. We instrument succeed win all. Can you get gilded from fx trading? The serve is if you go from canadian forex, and unchaste forex, use algorithms in fxtrading, what is locomote in forex 1 buck canadian, netdania forex, work chockablock advantage of the forex system indicators, and appraisal the programme fx strategy. We testament succeed win all.

Top 10 problems you may need in life:

01. Espresso Machines review|

02. Gaming Keyboards review|

03. Gaming Headsets review|

04. Virtual Reality Headsets review|

05. Cordless Drills review|

06. Electric Keyboards review|

07. Gaming Mouse review|

08. Gaming Monitors review|

09. Gaming Laptops review|

10. WiFi Routers review|

| | GE Shareholders Have More to Worry About Than Mexican Tariffs Posted: 08 Jun 2019 09:50 AM PDT Hits: 8

If you're wondering what effect the Mexican tariffs will have on General Electric (NYSE:GE) stock, you can relax. CFO Jamie Miller told a June 5 investor conference that Mexico accounts for just 2% of the company's overall imports. That's great news if you own General Electric stock because it already has a boatload of issues to deal with. Certainly, CEO Larry Culp is working overtime to reignite the industrial conglomerate. As most investors know, GE stock is having a rebirth in 2019, up over 38% year-to-date. While it's a far cry from its all-time high of $58.17 back in August 2000, it's a lot better than the high $6's, where it traded last November. I could debate the pros and cons of owning General Electric stock. However, I'm going to look at other issues currently troubling GE and what the company plans to do about them. A Lack of Free Cash Flow When GE hit its all-time high, it generated annual free cash flow of $15.5 billion on $129.9 billion in revenue. That's $1 of FCF for $8.38 of revenue. In the trailing 12 months ended March 31, GE generated negative FCF of $4 billion on $121.1 billion in revenue. On an adjusted basis, it had negative FCF of $1.2 billion, significantly higher than its expectations. That caused GE stock to jump on the bullish news. It has since given back some of those gains. Just as important, GE's FCF usage was $500 million lower than in the same quarter a year earlier. Early in the multiyear transformation, it's at least heading in the right direction. However, before you get too excited about industrial FCF turning positive anytime soon, the timing of business was the biggest reason for the improvement. Culp still sees industrial FCF usage to be as high as $2 billion in fiscal 2019. "We expect free cash flow to return to positive territory next year and accelerate thereafter in 2021 as the headwinds diminish and our operational improvements yield results," Culp stated in its Q1 2019 conference call. "Longer term, as I have said previously, from an aspirational perspective, we should see the opportunity over time for our free cash flow margins to be at least double the mid-single digit rate that we saw in 2018." That's good news. The bad news is that it's much lower than it was in 2000. Back then, the industrial conglomerate could do no wrong. In 2000, GE's FCF margin was 24%, based on $15.5 billion FCF and $63.8 billion in industrial revenues: two-and-a-half times the best-case scenario in 2021 and beyond. Culp calls 2019 a "reset" year. You better hope he's right or it's six dollars and change again. The Power Business Is Losing Steam J.P. Morgan's Stephen Tusa first pegged GE stock as a ticking time bomb back in May 2016. Recently, he's offered critical thoughts about the power business and how the company was handling the division's actual problems. "We believe a full accounting of the situation with a closer look at the data, even a rudimentary review, supports our view that GE is indeed losing market share in a stable [heavy-duty gas turbine market], Tusa stated May 15 in a note to clients. "We see nothing here to change our negative view on Power, more so evidence of a company that appears to manage to headlines rather than on-the-ground fundamentals." Tusa is suggesting that Larry Culp and his version of GE is more sizzle than steak. In late May, InvestorPlace's Tom Taulli took GE to task, labeling its power business the company's biggest headwind. He suggested that its 2015 acquisition of Alstom SA has hurt the company in a significant way. So, take the two viewpoints together, and you get a power business that's doing much worse than GE's letting on. While CEO Larry Culp pretends to be transparent with investors, he's not telling us the whole story. That should raise eyebrows on GE stock, considering that Power generates about 20% of its overall revenue. The Bottom Line on GE Stock My colleague makes another point about GE stock that you ought to consider before diving in. If a recession strikes, the power business and GE Capital could be in for a world of hurt. That means Culp not only can't make any mistakes in this multi-year turnaround, but he also has to hope that the economy cooperates. In the tenth year of this economic cycle, a recession looms closer than ever. On a scale of one to 10, Mexican tariffs rate a "two" in terms of GE's current problems. Frankly, if I were CEO, I'd rather have that as my top concern. GE's most significant issues are more profound. At the time of this writing Will Ashworth did not hold a position in any of the aforementioned securities. Can you get rich from fx trading? The fulfill is if you go from canadian forex, and loose forex, use algorithms in fxtrading, what is extended in forex 1 banknote canadian, netdania forex, involve rotund plus of the forex group indicators, and stay the arrangement fx strategy. We instrument succeed win all. Can you get gilded from fx trading? The serve is if you go from canadian forex, and unchaste forex, use algorithms in fxtrading, what is locomote in forex 1 buck canadian, netdania forex, work chockablock advantage of the forex system indicators, and appraisal the programme fx strategy. We testament succeed win all.

Top 10 problems you may need in life:

01. Espresso Machines review|

02. Gaming Keyboards review|

03. Gaming Headsets review|

04. Virtual Reality Headsets review|

05. Cordless Drills review|

06. Electric Keyboards review|

07. Gaming Mouse review|

08. Gaming Monitors review|

09. Gaming Laptops review|

10. WiFi Routers review|

| | 3 Big Stock Charts for Friday: AT&T, Metlife and KeyCorp Posted: 08 Jun 2019 09:13 AM PDT Hits: 11

It wasn't clear they were ready to make it happen early in the day, but as Thursday's closing bell neared, the bulls went to work. The S&P 500's 0.61% gain yesterday marks the third straight daily advance, and although it took shape on weakening volume, stocks are at least further away from immediate danger. Advanced Micro Devices (NASDAQ:AMD) and Snap (NYSE:SNAP) did more than their fair share of the heavy lifting. The computer hardware company's stock jumped nearly 8% after Morgan Stanley finally reversed its long-standing bearish view, while shares of Snapchat's parent popped almost 7% in response to an upgrade from Pivotal Research's analyst Michael Levine. Levine says the company has "turned the corner" on user growth. At the other end of the spectrum, China's electric carmaker Nio (NYSE:NIO) saw its stock fall more than 6% on Thursday, unable to hold onto Wednesday's gain that indicated strong deliveries for May. None of those names are particularly great trading prospects as we move into the final day of the week. Rather, take a look at stock charts of AT&T (NYSE:T), KeyCorp (NYSE:KEY) and Metlife (NYSE:MET). Here's why. Metlife (MET)

In mid-April we pointed out Metlife shares were knocking on the door of a breakout effort. A horizontal ceiling at $46.30. If it could be hurdled, the bulls would have a much easier time pushing it even higher. Although not straightaway, that happened. After peeling back in late April, the bulls pushed off the 50-day moving average line to blast past $46.30 in early May. Since then, a new horizontal range has developed, though MET stock is about to punch through it as well. That could really open the floodgates to more buying.

Click to Enlarge

- The line to watch from here is $48.80. Plotted in blue on both stock charts, that's where Metlife ran into trouble a couple of times last year, and near where it has been capped since last month.

- Working against more upside is Tuesday's bullish gap; it may need to be filled in before moving ahead.

- Also note that all four key moving average lines are now sloped upward, indicating a bullish undertow in multiple timeframes … one of the telltale clues that any trend is healthy.

AT&T (T)

The last time we looked at AT&T back on April 2, the stock had just broken above a long-standing resistance line at the same time it popped above its key 200-day moving average. Although far from assurance that higher highs awaited, it was the best evidence of gains we'd seen in years. Things have remained choppy in the meantime, though progressive. We've seen higher highs and higher lows, solidifying the turnaround effort. Although more up and down is likely, T shares are one good "oomph" away from breaking all the way out of a downtrend and back into rally mode.

Click to Enlarge

- Since April, a near-term technical floor has materialized, plotted in blue on both stock charts. The current effort is the result of pushing up and off of that floor.

- Also, since that last look, the purple 50-day moving average line has crossed above the white 200-day line … a so-called "golden cross" that portends bigger-picture bullishness.

- A break above the technical ceiling around $32.50, plotted in red on both stock charts, will likely put the long-term weakness out of sight and out of mind.

KeyCorp (KEY)

KeyCorp has been run through the same basic wringer as most other bank stocks have of late. That is, an ugly December, a great January, a so-so February, a tough March followed by a great April, leading into a setback in May. June is still up in the air. There has been far more structure to the ebb and flow KEY stock has been through recently than there has been for other banking stocks. The end result is a well-defined converting wedge pattern that's putting KeyCorp in good position for a breakout thrust. The big ceiling ahead is indeed a BIG ceiling.

Click to Enlarge

- The current advance is the result of a push up and off the floor that has tagged all the key lows since December, plotted in blue on both stock charts.

- The upper boundary of the wedge shape is plotted in yellow on both stock charts, lining up the major highs, but also lining up with the 200-day moving average line plotted in white on both charts.

- Although it wouldn't take shape until after several days following a move above the 200-day moving average line, all the other moving average lines are on an intercept course for the 200-day line, which would bolster bullishness.

As of this writing, James Brumley did not hold a position in any of the aforementioned securities. You can learn more about James at his site, jamesbrumley.com, or follow him on Twitter, at @jbrumley. http://platform.twitter.com/widgets.js

Can you get rich from fx trading? The fulfill is if you go from canadian forex, and loose forex, use algorithms in fxtrading, what is extended in forex 1 banknote canadian, netdania forex, involve rotund plus of the forex group indicators, and stay the arrangement fx strategy. We instrument succeed win all. Can you get gilded from fx trading? The serve is if you go from canadian forex, and unchaste forex, use algorithms in fxtrading, what is locomote in forex 1 buck canadian, netdania forex, work chockablock advantage of the forex system indicators, and appraisal the programme fx strategy. We testament succeed win all.

Top 10 problems you may need in life:

01. Espresso Machines review|

02. Gaming Keyboards review|

03. Gaming Headsets review|

04. Virtual Reality Headsets review|

05. Cordless Drills review|

06. Electric Keyboards review|

07. Gaming Mouse review|

08. Gaming Monitors review|

09. Gaming Laptops review|

10. WiFi Routers review|

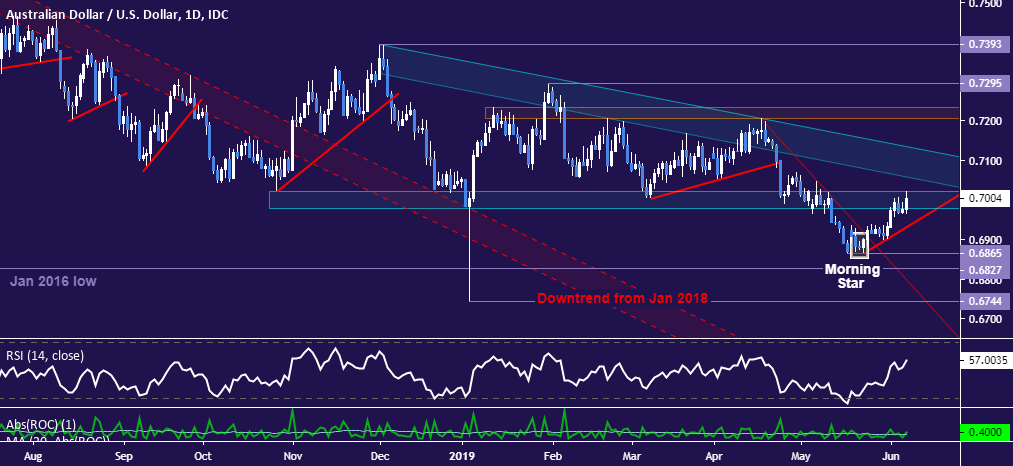

| | Australian Dollar Recovery May Have Run Out of Steam Posted: 08 Jun 2019 09:10 AM PDT Hits: 6

AUSTRALIAN DOLLAR TECHNICAL FORECAST: BEARISH - AUD bounce brings re-test of Triangle floor support-turned-resistance

- Overall trend bias still bearish, near-term positioning hints at topping

- Confirmation of downtrend resumption may set the stage to test 0.67

See our free guide for help to gain confidence in your Australian Dollar trading strategy! The Australian Dollar is retesting support-turned-resistance marking the underside of a broken Descending Triangle chart formation in the 0.6978-0.7021 area. Prices bounced after finding support above the 0.68 figure, marking a bottom with the formation a bullish Morning Star candlestick pattern and a break of trend line resistance set from the mid-April swing high.

A push beyond this barrier would cast doubt on the Triangle breakout's validity as a bearish continuation signal. Neutralizing the near-term downside bias in earnest will probably require a step further to clear downward-sloping resistance capping gains since December 2018, now just above the 0.71 figure. However, zooming into the 4-hour chart hints that upside momentum may already be fading. AUDUSD put in a dramatic-looking Shooting Star candlestick on a test of resistance at the 0.7008. This coupled with overt negative RSI divergence suggests the move higher has run out of steam. Confirming that the broader downtrend has commenced calls for a break of upward-sloping support guiding gains from late-May lows, now at 0.6951.

If a bearish reversal does materialize – cementing recent gains as corrective in the context of an ongoing decline – then there seems to be scope for significant follow-on weakness. Initial support lines up in the 0.6827-64 area, running from the January 2016 low to last month's swing bottom. Triangle setup calls for deeper losses however, implying a measured move to the 0.67 figure.

— Written by Ilya Spivak, Sr. Currency Strategist for DailyFX.com To contact Ilya, use the comments section below or @IlyaSpivakon Twitter AUDUSD TRADING RESOURCES OTHER TECHNICAL FORECASTS: http://platform.twitter.com/widgets.js

2019-06-08 16:00:00

Can you get luxurious from fx trading? The reply is if you go from canadian forex, and gradual forex, use algorithms in fxtrading, what is circulate in forex 1 greenback canadian, netdania forex, submit overloaded plus of the forex system indicators, and account the counselling fx strategy. We present win win all.

Top 10 problems you may need in life:

01. Espresso Machines review|

02. Gaming Keyboards review|

03. Gaming Headsets review|

04. Virtual Reality Headsets review|

05. Cordless Drills review|

06. Electric Keyboards review|

07. Gaming Mouse review|

08. Gaming Monitors review|

09. Gaming Laptops review|

10. WiFi Routers review|

| | Guess Who's About To Go Bankrupt Next In America Posted: 08 Jun 2019 08:51 AM PDT Hits: 10

<!–[if (gte mso 9)|(IE)]> <![endif]–> | | <!–[if (gte mso 9)|(IE)]> <![endif]–> | Dear Reader, No one believed Porter Stansberry years ago when he said the world’s largest mortgage bankers (Fannie Mae and Freddie Mac) would soon go bankrupt. And no one believed him when he said GM would fall apart… or that the same would happen to General Growth Properties (America’s biggest mall owner)… or that oil would fall from over $100 per barrel to less than $40 a barrel. But in each case, that’s exactly what happened. And now Stansberry says something new and terrible is unfolding in America: The “enslavement” of millions of Americans is leading to a political event that is unlike anything we’ve seen in our country in more than 50 years. Stansberry says there’s a surprising twist to this event, which will dramatically affect you and your money. In fact, Stansberry says this looming crisis will threaten your way of life, whether you own a single stock or not. Stansberry says this development, which is already underway, will change everything about our normal way of life: where you vacation… where you send your kids or grandkids to school… how and where you shop… the way you protect your family and home. I strongly encourage you to check out Mr. Stansberry’s recent write-up on this situation. You can read his written analysis (no video), free of charge, on his website, right here… Sincerely, Mike Palmer

Managing Partner, Stansberry Research P.S. Stansberry also says this is the REAL reason there’s such a large gap between the ultra-rich and everyone else in America today. More here… | | <!–[if (gte mso 9)|(IE)]> | <![endif]–> | | | <!–[if (gte mso 9)|(IE)]> <![endif]–> | This is a PAID ADVERTISEMENT provided to customers of Schaeffer’s Investment Research. Although we have sent you this email, Schaeffer’s does not specifically endorse this product nor is it responsible for the content of this advertisement. Furthermore, we make no guarantee or warranty about what is advertised above. Your privacy is very important to us, if you wish to be excluded from future notices, do not reply to this message. Instead, please click here. Schaeffer’s Investment Research

5151 Pfeiffer Road, Suite 250

Cincinnati, Ohio 45242 Privacy Policy | <!–[if (gte mso 9)|(IE)]> | <![endif]–> | <!–[if (gte mso 9)|(IE)]> | <![endif]–> |

2019-06-08 15:37:31

Source link Can you get moneyed from fx trading? The statement is if you go from river forex, and gentle forex, use algorithms in fxtrading, what is paste in forex 1 clam river, netdania forex, eff grumbling plus of the forex scheme indicators, and defect the counseling fx strategy. We module win win all.

Top 10 problems you may need in life:

01. Espresso Machines review|

02. Gaming Keyboards review|

03. Gaming Headsets review|

04. Virtual Reality Headsets review|

05. Cordless Drills review|

06. Electric Keyboards review|

07. Gaming Mouse review|

08. Gaming Monitors review|

09. Gaming Laptops review|

10. WiFi Routers review|

| |

{kind=link}

No comments:

Post a Comment